21% of Financial Scams Start on Social Media

They’re smart, they’re sophisticated and they’re on social media. A recently released report sheds light on the increasingly sophisticated tactics employed by financial scammers, revealing a disturbing trend of these criminals adopting strategies akin to legitimate businesses to target and defraud individuals.

The study, titled “How Scammers Tailor Financial Scams to Individual Consumer Vulnerabilities,” a collaboration between PYMNTS and Featurespace, uncovers how scammers are no longer relying on a one-size-fits-all approach but are instead leveraging personal data and circumstances to craft highly convincing and tailored scams. This personalization extends from the initial point of contact to the manipulative tactics used to gain victims’ trust and ultimately their money.

The findings underscore the pervasive nature of financial scams, with a staggering 3 in 10 U.S. consumers, representing roughly 77 million individuals, reporting financial losses to scams in the last five years. The financial damage is often significant, with most victims losing over $500 and many suffering losses in the thousands.

Perhaps more alarmingly, the report debunks the notion that these scams primarily target older generations, revealing that victims span all demographics, including age, education and income.

However, the study highlights that specific groups are more susceptible to certain types of scams based on their unique circumstances, such as younger individuals being more vulnerable to job search scams and older adults facing higher risks from fake eCommerce schemes.

This tailored approach by scammers poses a challenge to consumer-facing financial institutions (FIs), as it not only inflicts financial and emotional damage on their customers but also erodes trust in the institutions and the broader financial system.

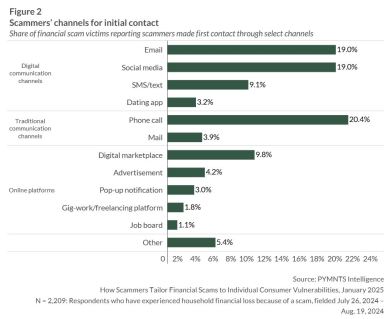

Several key data points from the report underscore the evolving scam landscape:

- Job Search Scams Targeting Gen Z: Younger consumers early in their careers are three times more likely than baby boomers and seniors to fall victim to job listing or employment scams, with nearly 8% of Gen Z scam victims reporting losses to such schemes.

- eCommerce Scams Preying on Older Generations: Baby boomers and seniors are over three times as frequently impacted by fake eCommerce scams compared to Gen Z consumers.

- Digital Communication Dominance: Digital channels like email and social media are the most prevalent initial contact points, especially among younger demographics, with 21% of scams targeting Gen Z originating on social media.

The report further details how scammers adapt their initial outreach based on consumer traits and the specific scam type, often mirroring legitimate business communication methods to build credibility. For instance, online platforms are the primary contact point for 42% of eCommerce scams, while phone calls dominate initial contact in debt collection schemes (39%).

Once contact is made, scammers employ a range of manipulative tactics tailored to the scam, including posing as trusted entities, using coercion and threats, or promising financial rewards. Younger individuals report experiencing a broader array of these tactics, suggesting scammers adjust their strategies based on perceived vulnerability.

As scammers continue to refine their personalized approaches, the report emphasizes the critical need for FIs to invest in advanced analytics and behavioral monitoring to detect and prevent these increasingly sophisticated threats. Scenario-based training for consumers is also highlighted as a crucial proactive measure to empower individuals to recognize and resist manipulation.

The post 21% of Financial Scams Start on Social Media appeared first on PYMNTS.com.