26% of Consumers Leave Credit Cards Due to Payment Challenges

Consumers’ relationships with credit are shaped by various life circumstances, which influence their decisions to enter or leave the credit market.

A PYMNTS Intelligence report, What Causes Credit Card Users to Leave the Market — and How Secured Cards Can Win Them Back, in collaboration with Atelio, unveils differences in the reasons why high- and low-income consumers step away from credit products. While both groups show interest in returning, the path forward for each is distinct.

Secured credit cards offer tailored solutions for both, addressing unique financial needs. The report explores how financial institutions (FIs) and credit issuers can use secured cards to attract credit card outsiders back into the market.

Income-Based Motivations

One of the main reasons consumers leave the credit market is due to difficulty managing payments, but the experience differs between income brackets. Among credit card outsiders, 26% cite payment challenges as the primary reason for closing their accounts. For low-income consumers, this concern is more pronounced, with 32% reporting payment struggles, compared to just 20% of high-income consumers.

High-income consumers, on the other hand, often leave credit cards due to preference for other payment methods, such as accumulated wealth or alternative credit sources. While only 2% of low-income consumers closed their accounts for this reason, 19% of high-income consumers made this decision. These differences underscore the need for tailored solutions for each income group.

For low-income consumers, secured cards offer relief from financial strain by providing controlled spending limits linked to collateral, which can help manage monthly balances effectively. With unexpected events like job loss amplifying financial strain, secured cards can serve as a safeguard.

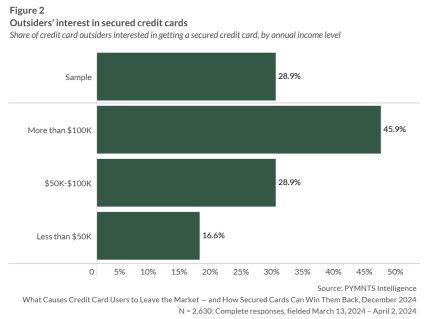

High-income consumers, however, are more likely to seek added value through features like rewards programs and flexible payment options. Secured credit cards can cater to this need by offering benefits that complement their existing financial portfolios. Consider 46% of consumers earning more than $100,000 annually express interest in secured credit cards, indicating potential for high-income engagement.

Supporting Outsiders Through Life ChangesLife events such as illness or job loss disproportionately impact low-income consumers, making them more vulnerable to financial strain. In fact, 27% of low-income consumers report that employment changes negatively affected their finances, compared to a smaller share of high-income consumers. For these individuals, secured credit cards can provide access to emergency credit during unpredictable life events, offering both financial stability and peace of mind.

In contrast, high-income consumers face challenges from planned expenses, such as moving or education costs. While these events can be anticipated, they still require careful financial management. Secured cards can assist high-income consumers by offering tools like adjustable credit limits and budgeting features, helping them manage large but expected expenses.

The post 26% of Consumers Leave Credit Cards Due to Payment Challenges appeared first on PYMNTS.com.