48% of Gen Z Would Boost Primary Card Use With Better Payment Features

In the fiercely competitive world of consumer credit, securing a “top-of-wallet” position is not merely a preference but a determinant of an issuer’s financial health and profitability.

[contact-form-7]PYMNTS Intelligence’s May 2025 report, “The Credit Economy: Top-of-Wallet Credit Cards,” produced in collaboration with i2c, details consumer preferences and behaviors influencing primary credit card selection and usage. The research, based on a survey of 2,275 consumers conducted from March 4 to March 31, 2025, reveals how achieving top-of-wallet status is crucial for issuers’ bottom lines.

Primary cards generate much more revenue for issuers, with U.S. consumers using their preferred cards heavily, carrying an average monthly balance of nearly $2,000. This contrasts sharply with second-choice cards, which average just over $1,200, and third-place cards, at more than $900.

The report underscores that this top-of-wallet dynamic intensifies when consumers hold multiple cards. These individuals tend to concentrate their spending on one primary card, rather than distributing it evenly across their accounts, particularly for routine purchases. This makes top-of-wallet status a particularly valuable prize for issuers seeking to maximize transaction fees, interest (APR), and other consumer-borne fees.

Key findings from the report include:

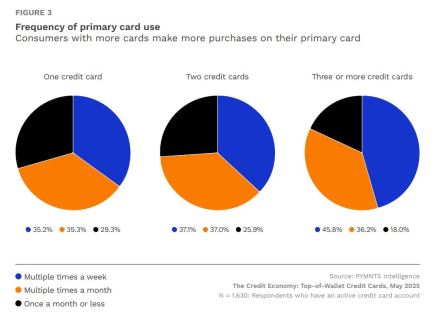

- Frequent Primary Card Use With Multiple Cards: Consumers possessing more credit cards exhibit a higher frequency of primary card usage. Specifically, 46% of cardholders with three or more cards use their primary card multiple times a week, compared to 37% of those with two cards and 35% of those with just one. This trend highlights the importance for issuers to secure this position, especially as nearly half of all credit cardholders own three or more cards.

- Younger Consumers’ Reliance on Primary Cards and Demand for Control: Gen Z and millennials demonstrate a greater reliance on their primary cards, utilizing a higher average percentage of their credit limits. Gen Zers, on average, use 30% of their top-of-wallet card’s credit limit, followed by millennials at 27%, while Gen X and baby boomers use 19% and 16% respectively. Furthermore, younger consumers, particularly Gen Z (48%) and millennials (41%), express strong interest in increasing primary card usage if offered more payment control options at the time of purchase, such as monthly installments or immediate full payment. They also show a greater desire for higher credit limits and issuer-provided insights into spending.

- Rewards as a Dominant Motivator: Rewards and discount programs stand out as the most significant motivation when consumers select a primary credit card. While 48% of cardholders cite rewards or discounts as a key factor in choosing their primary card, 31% identify it as the single most important reason. This emphasis on rewards is particularly strong for those who primarily use their cards for everyday spending.

Beyond these critical data points, the report also examines how card ownership varies by age and income levels, with younger consumers generally holding fewer cards but relying more heavily on their primary ones. It explores the differing reasons for card choice based on typical usage — for instance, low interest rates are prioritized for emergency use, while security features are key for bill payments.

These insights reinforce the importance for issuers to tailor their credit card products and features to specific target consumer profiles, optimizing their appeal and increasing the likelihood of securing top-of-wallet status.

The post 48% of Gen Z Would Boost Primary Card Use With Better Payment Features appeared first on PYMNTS.com.