63% of Americans Now Use Digital Wallets for Cross-Border Payments

The digital divide that once separated who paid how across borders is narrowing fast. In the United States, digital wallets have become the great equalizer. They’re used almost as readily by retirees as by recent college graduates, and by middle-income consumers as by the wealthy.

That’s the subtle but striking finding in “Global Money Movement: U.S. Edition,” an April 2025 data brief by PYMNTS Intelligence. The report shows that digital wallets, once viewed as tools for tech-savvy youth or affluent travelers, have quietly become a mainstream mechanism for sending and receiving money internationally. Nearly two-thirds of U.S. cross-border payers — 63% — now use them.

This even spread, across age and income lines, may prove more consequential than raw adoption numbers. It suggests that digital wallets are no longer just a payment technology; they are becoming an infrastructure for financial inclusion in cross-border commerce. It’s one where convenience, not demographics, defines participation.

Among the Findings:

- Generational parity: Millennials (68%) and Gen X (70%) are the most active users of digital wallets for international payments, but boomers and Gen Z are close behind at 48% each — a rate nearly identical across the oldest and youngest adult cohorts.

- Income equality: Two-thirds (66%) of Americans earning over $100,000 a year use digital wallets for cross-border transactions — but so do 54% of those making under $50,000. The technology’s appeal cuts across financial brackets.

- SMB hesitation: By contrast, only 48% of U.S. small and medium-sized businesses (SMBs) use digital wallets for international transactions, and one in three non-users say the method’s lack of industry-standard status keeps them from adopting it.

Together, these figures sketch a picture of a consumer market that has normalized digital wallets — and a business market that hasn’t caught up. While consumers see wallets as secure and convenient as debit cards or bank transfers, many SMBs still cite security concerns or limited interoperability as reasons for staying on the sidelines.

That hesitation may prove costly. Speed is emerging as the killer feature on both sides of the transaction. The report finds that 54% of U.S. consumers who do not yet use digital wallets cite faster settlement as their top reason to start within the next year, while 40% of merchants not yet on board name speed as their leading motivator. The alignment between senders and receivers hints at a market-wide tipping point: once the business infrastructure catches up, usage could surge.

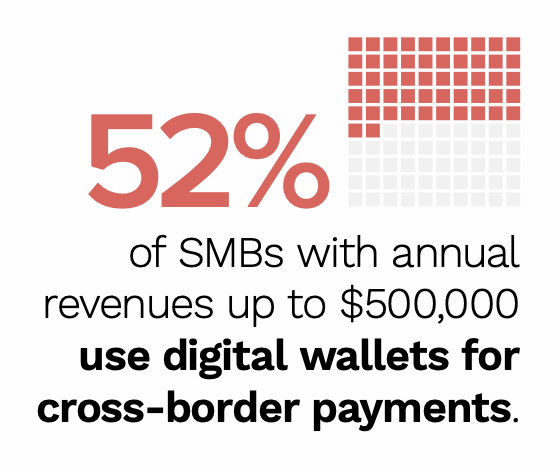

Other findings reinforce the idea that the U.S. is maturing into a digital-wallet-driven remittance and trade environment. Americans’ familiarity with the technology (64%) now rivals that of credit and debit cards, and small businesses with annual revenues under $500,000 actually lead larger peers in adoption (52% versus 46 %).

The broader implication is that digital wallets are erasing the demographic boundaries that once defined financial behavior. The same device that a Gen Z freelancer uses to pay an overseas designer is helping a retiree send money to family abroad. For policymakers and payment providers, that convergence signals an opportunity — and a responsibility — to set clearer standards and strengthen security so that the next wave of adoption can extend beyond convenience toward confidence.

The post 63% of Americans Now Use Digital Wallets for Cross-Border Payments appeared first on PYMNTS.com.