BNPL, Mobile Banking Embraced by Low-Income, Paycheck-to-Paycheck Consumers

PYMNTS Intelligence’s long-standing chronicling of the paycheck-to-paycheck economy has revealed shifts in how consumers conduct their daily financial lives and pay.

Given that the paycheck-to-paycheck designation blankets roughly two-thirds of consumers, the changes have been widespread. Households continue to embrace digital, specifically mobile, channels for banking and account access, and they use buy now, pay later (BNPL) options as they transact.

In terms of connectivity, the 2024 PYMNTS Intelligence report “How the World Does Digital” found that 49.7% of consumers surveyed said they had engaged with mobile banking on at least a weekly basis. A lower percentage said they had done the same, at 46.7%, with online banking. That translates to total annual activity days of 26 days for high-income earners (generally, those earning above $100,000), 23 days for middle-income consumers ($50,000 to $100,000) and 18 days for low-income consumers (below the $50,000 threshold).

Mobile MomentumEvery so often, reports from government and other agencies reinforce PYMNTS’ findings on how technology and innovations are changing the way households consider and use financial products and services.

Such is the case this month with the Federal Deposit Insurance Corp.’s latest biennial Household Survey (tracking 2023), officially titled “National Survey of Unbanked and Underbanked Households.”

The FDIC found that more than 96% of households are banked. That means they had access to at least some traditional financial services products, such as checking or savings accounts. As many as 14% of households were considered underbanked, so they had accounts with traditional financial institutions but also used nonbank products to meet their financial needs.

As for the data that squares up with PYMNTS’ findings amid the wide embrace of digital channels, the FDIC found that 48.3% of banked households used mobile banking as their primary method of account access. About half of all households, at 49.7%, used online payment services, up more than three percentage points from 2021.

BNPL and Credit

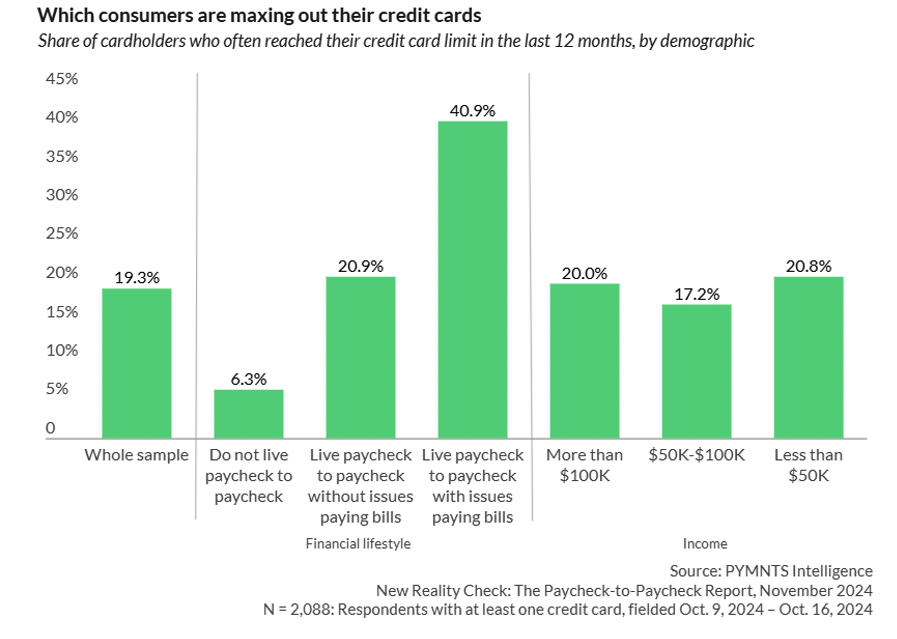

Mainstream credit — i.e., the use of credit cards — remains prevalent. PYMNTS Intelligence found that 74% of all consumers carry at least some credit card debt. The FDIC found that about 70% of underbanked households and 80% of banked households had cards, indicating a range that corroborates what the paycheck-to-paycheck economy told PYMNTS. Three-quarters of all income levels we surveyed carried a balance. Among low-income households — where our data showed that roughly 80% of households live paycheck to paycheck — 21% hit their credit card spending limits through the past year. An increasing percentage of households are turning to installment plans to help meet their financial needs.

The FDIC’s survey said that 3.9% of all households used BNPL options through the past 12 months. A larger share of households with income between $30,000 and $50,000 (4.7%) or between $50,000 and $75,000 (4.8%) used BNPL.

PYMNTS Intelligence found that paycheck-to-paycheck consumers are more than twice as likely as non-paycheck-to-paycheck consumers to use BNPL. Thirty-eight percent of consumers earning between $50,000 and $100,000 and 29.6% of those earning below $50,000 used BNPL through the preceding 12 months.

The post BNPL, Mobile Banking Embraced by Low-Income, Paycheck-to-Paycheck Consumers appeared first on PYMNTS.com.