Card Delinquencies Hit Multiyear High

The holiday splurge has passed — and now comes the holiday hangover?

The New York Federal Reserve detailed in its most recent report, “Household Debt and Credit,” that consumers loaded up on their credit cards in the fourth quarter of the year — which encompassed the holiday shopping season lasting through November and December. Card balances surged by $45 billion, even while delinquency rates are, per the Fed’s language, “elevated.”

The pressures of new debt, added to debt that already was in delinquency, along with inflation that’s pushing consumers to keep using their credit card, all point to a tougher time meeting the obligations of that debt, much less paying it down.

The headline numbers of the report indicated that total household debt increased by $93 billion (0.5%) in the fourth quarter, to $18.04 trillion. In relative terms, this is the mildest increase of the year, following rises of 0.8% and 0.6% respectively in the third and second quarters of last year. The increase relative to the same quarter of 2023 amounts to $53 billion, or 3%, very much in line with the percentage increase for consumer prices over the same period, as reported this week by the Bureau of Labor Statistics.

A Buildup of Card DebtBut credit card debt drove roughly 48% of the overall quarterly increase that was noted above. Credit card debt reached $1.2 trillion at the end of December.

The 3.9% quarterly increase in card balances was the strongest of the year, on the back of 2.1% and 2.4% respectively in the two prior quarters. Card debt is also growing more quickly, as balances increased by 7.3% year over year.

In comparison, auto loans and mortgages grew by 2.9% and 3% year over year.

Delinquencies Are GrowingAt a high level — and in looking at consolidated debt — delinquency rates increased slightly from the previous quarter, with 3.6% of outstanding debt in some stage of delinquency.

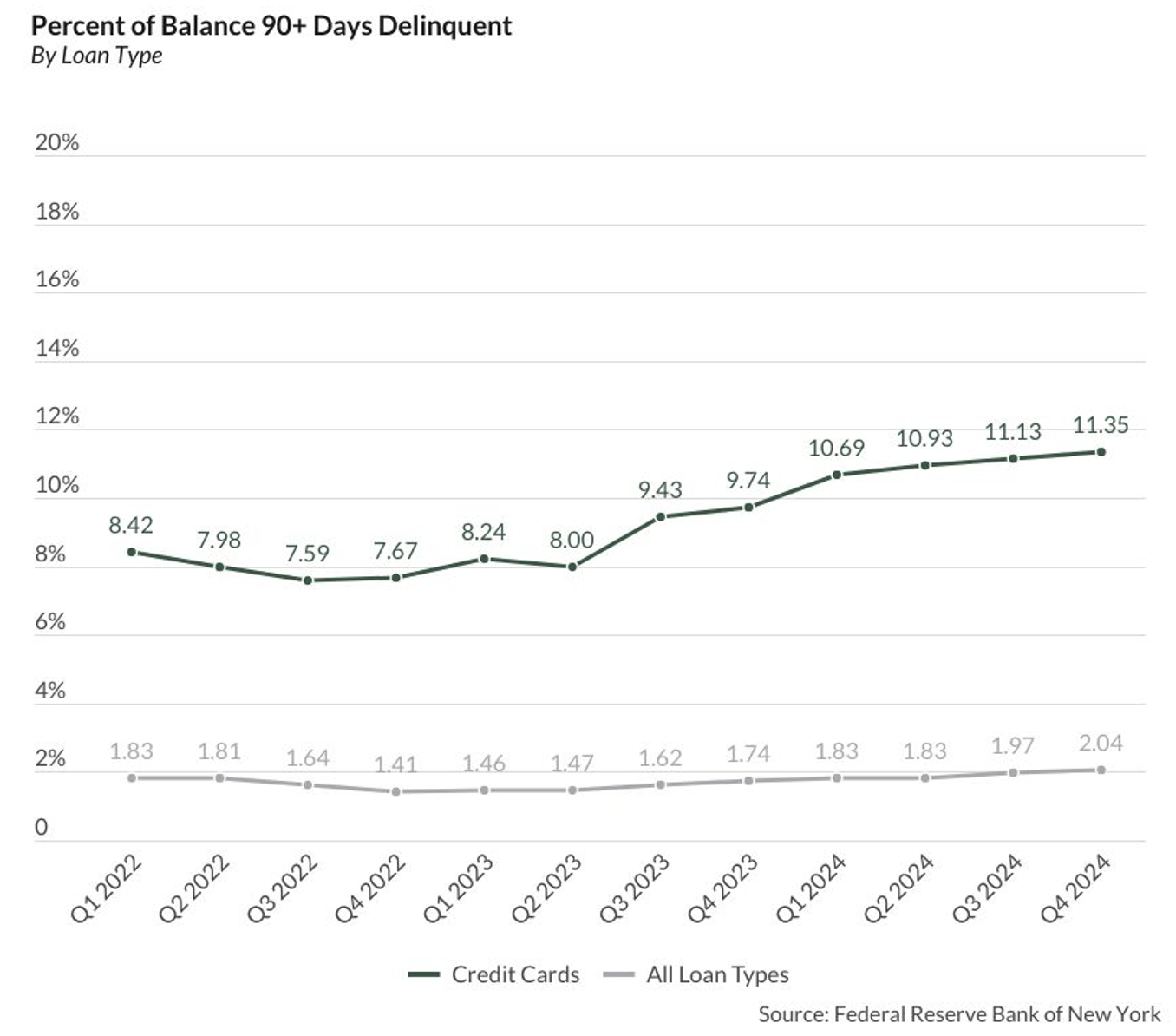

But credit cards continue to be the loan type with the highest share of balance 90+ days delinquent, at 11.35%. This share grew 2% quarterly and 17% year over year.

We haven’t seen these levels of delinquency in years — and in fact, not since the fourth quarter of 2011.

There are some indications that consumers may run out of runway, so to speak; the Fed reported that aggregate limits on credit cards increased moderately, by $98 billion or 2% quarter-on-quarter.

As PYMNTS Intelligence found in November, as consumers headed into that all-important shopping season, a significant percentage of consumers were already moving toward or hitting their credit card limits. As detailed here, 41% of financially struggling cardholders often or always reach their limits. Of all consumers surveyed, more than 19% had “often” met their limits in the past 12 months.

And lest you think that high-earning households are immune from the pressures of card debt, consider the fact that 20% of households queried by PYMNTS Intelligence signaled that they often bumped up against their spending limits.

Consumers have been reaching for their cards to pay for everyday essentials such as groceries. In that one particular category, inflation has been reaccelerating, as measured in the January CPI data. An interest-rate-cut pause from the Fed means that credit card interest rate charges are not likely to lessen any time soon — making it that much harder to manage the debt that’s on the books.

The post Card Delinquencies Hit Multiyear High appeared first on PYMNTS.com.