Issuers Want Core Banking and Processing Relationships With a Single Provider

For card issuers seeking to modernize and digitize, there’s a strong preference to have a go-to provider as a single point of access for critical functions, PYMNTS Intelligence data show.

[contact-form-7]As we conducted our surveys of payments professionals for the joint report done between PYMNTS Intelligence and Visa DPS, titled “The Best-In-Class Modern Card Issuer: Driving Customer Lifetime Value Through Innovation,” a few key trends emerged. Card issuance has become a competitive advantage for smaller financial institutions (FIs) and even FinTechs and (as has always been the case) larger banks.

But to get there, and to capitalize on the ongoing digital shift that includes the issuance of virtual cards, among other innovations, the back-end processes to facilitate transactions and to remain in compliance with regulatory mandates must be upgraded.

Modernization is no easy task, as a rip and replace of extant systems, some of them decades old, would stop operations in their tracks.

Relying on core banking services providers for these back-end efforts — tied to accounts — along with ancillary payments processing speeds time to market with those aforementioned providers.

More Modernization Means More RevenuesThe PYMNTS Intelligence/Visa data show that high-performing issuers leverage more than seven “modernization methods” that move beyond simple transactions to expand into new features in order to maximize customer lifetime value. We wrote, in example of those modernization efforts that “automated issuance to a digital wallet and account upgrades are among the many types of issuances high-CLTV issuers offer more often the average issuer, adding to their portfolio of monetizable products.”

The push toward new revenue streams is by no means confined to banks, and in many cases FinTechs are accelerating their own efforts to move more firmly into what be called traditional financial services.

PYMNTS Intelligence and Visa DPS also found that 29% of high-CLTV FinTechs offer single-use virtual cards and embedded card issuance, compared to 14% and 11%, respectively, for high-CLTV banks. Instant issuance and single-use virtual cards serve as key differentiators.

In seeking an issuer partner with which to link up, the banks and FinTechs have listed their key considerations. Data shows that high CLTV issuers choose partners that offer advanced security features and flex credentials.

Partnership PotentialFor the platforms and providers that offer a broad range of solutions, it should be noted that our “best in class” surveys found that approximately 3 in 10 issuers surveyed cite difficulty integrating with other systems and limited customization options as pain points they have experienced with their current card issuing platform.

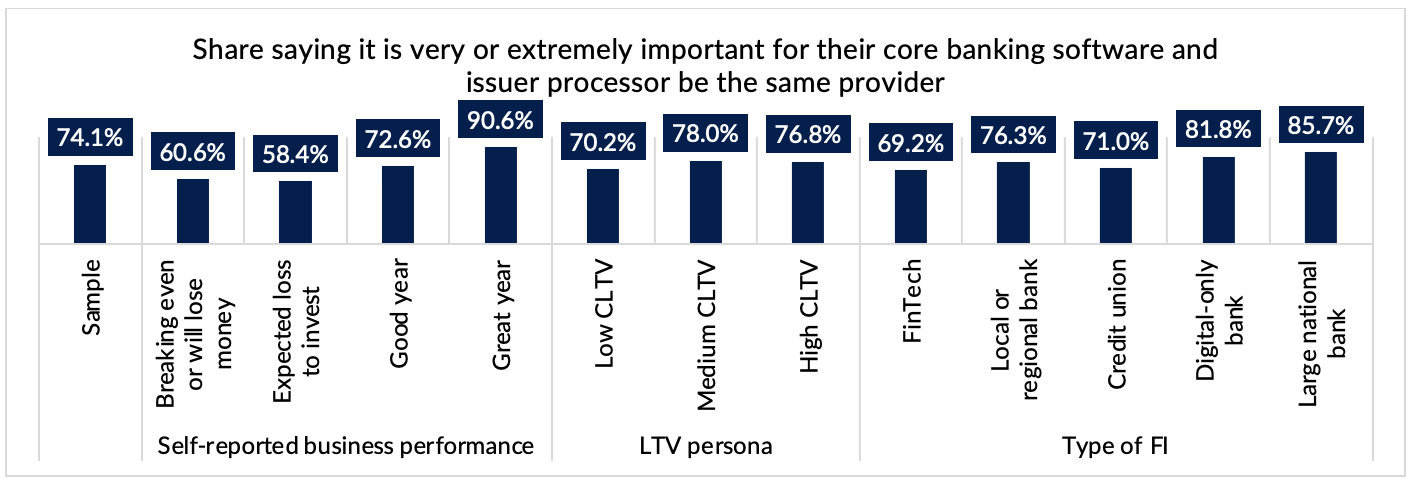

The chart below shows that when it comes to tapping into those solutions, the financial services firms would like to have what amounts to a one stop shop. Three-quarters of all firms surveyed said it is “very or extremely” important for the same (single) provider to be the core banking software vendor and issue processor.

That’s especially true with FIs and FinTechs, which are already doing well, and are already enjoying the fruits of long-lived customer relationships. Roughly three quarters of the more than 450 financial services providers queried said they preferred transaction pricing.

For providers, such as SoFi, or Visa, through its Pismo acquisition, growth has been strong. SoFi, for example, said in its latest quarter that the tech platform segment, which includes core banking, saw sales growth of 10% year over year. Visa closed its deal to acquire Pismo at the beginning of last year to provide clients with core banking and card-issuer processing capabilities across all product types via cloud-native application programming interfaces (APIs).

The post Issuers Want Core Banking and Processing Relationships With a Single Provider appeared first on PYMNTS.com.