Millennials Drive Demand for Flexible Card Payments

For decades, credit cards have remained remarkably unchanged in their core functionalities: swipe, spend, earn points.

[contact-form-7]But what was once revolutionary may have now reached a saturation point. Nearly every major issuer provides points-based rewards, tiered interest rates and fraud protection. These features can often no longer differentiate in a crowded market.

But a new wave of innovation is reshaping the consumer wallet, thanks to a simple but powerful shift: user customization. The PYMNTS Intelligence report “The Credit Economy: Top-of-Wallet Credit Cards,” a collaboration with i2c, reveals 40% of millennials and 48% of Gen Z consumers would increase their card usage if they could choose repayment plans at the point of sale.

That’s not just a preference; it’s a signal. As younger, tech-savvy users seek more control over their financial tools, banks, credit unions and FinTechs are responding with card products that behave more like digital platforms — malleable, data-driven and personal.

The Personalization ImperativeConsumers, particularly digital-first ones, want their cards to think like them, budget like them and even feel like them. Customizable cards are not about bells and whistles. They represent a paradigm shift: from one-size-fits-all finance to dynamic, user-driven design.

And as cardholders grow more sophisticated and digitally native generations enter their financial prime, the demand for cards that flex to meet individual needs is reaching critical mass.

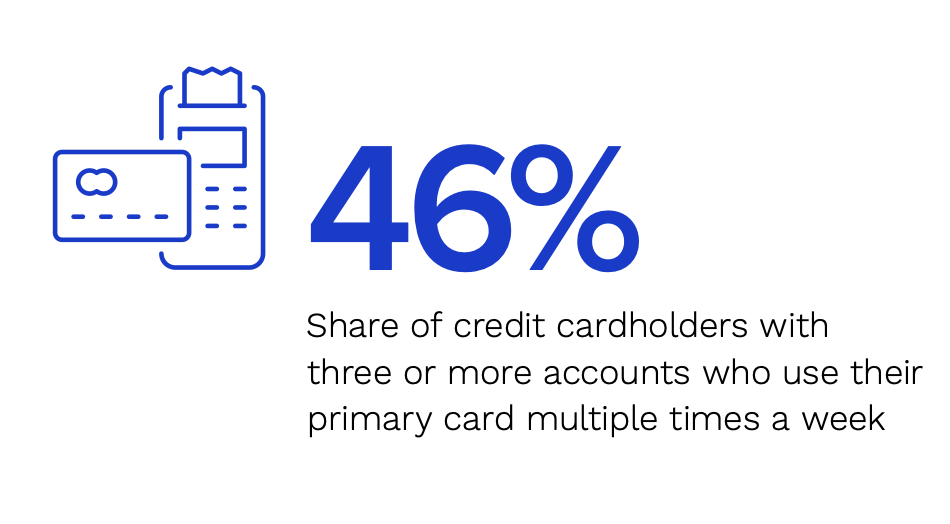

Primary cards, it turns out, matter most. While 78% of all credit cardholders have multiple cards, those with multiple cards overwhelmingly funnel spending toward just one. And that primary card? It delivers nearly $1,900 per month in balances — more than 50% higher than the second-choice option. Customization, in this context, isn’t just a UX upgrade. It’s a revenue strategy.

Still, if rewards got cards into wallets in the 2010s, they’ll need to evolve to stay there in the 2020s. Nearly half (48%) of consumers still rank rewards and discounts as their top motivator in selecting a primary card, but the definition of “rewarding” is changing. Today’s users want to feel like the card is helping them live better, not just spend more.

The PYMNTS and i2c data backs this up: consumers who use their cards primarily for everyday purchases — currently the most common usage pattern — are most likely to prioritize flexible rewards. Conversely, those who use cards for emergencies place greater emphasis on interest rates and credit access.

This behavioral segmentation may demand a flexible feature set, not a one-size-fits-all pitch.

Read the report: The Credit Economy: Top-of-Wallet Credit Cards

Gen Z and Millennials Want More ControlPerhaps the most disruptive finding is younger consumers’ desire for greater control over payments and spending. The PYMNTS Intelligence data, in collaboration with i2c, also revealed that 13% of consumers would use their primary cards more frequently if issuers provided deeper insights into card usage. Another 12% want the ability to pre-set spending limits or rules.

This points to a significant opportunity for financial innovation. Credit cards, once static instruments, are increasingly becoming platforms for personal finance management. Issuers who offer dashboards, nudges and smart controls may find themselves winning loyalty by helping users stay on top of their money, not just spend it.

As the payment ecosystem becomes more complex and consumer expectations more demanding, the fight for wallet supremacy will grow sharper. Credit cards are no longer simply tools for borrowing — they are now utilities, advisors and lifestyle enablers.

So, what’s next? Expect deeper integration with users’ lives such as smart cards that adjust categories based on health goals, or artificial intelligence (AI) that enables a vision blending convenience, control and care.

The PYMNTS and i2c report makes one thing abundantly clear: Issuers who embrace this evolution — blending financial utility with digital intimacy — will be the ones whose cards don’t just land in wallets but stay at the top.

The post Millennials Drive Demand for Flexible Card Payments appeared first on PYMNTS.com.