Why Economies Need People Willing to Stick Their Necks Out

To prosper, economies need catalysts. Catalysts aren’t just entrepreneurs with bright ideas. They’re people who stick their necks out when the odds are long and paybacks are uncertain.

But every great advance starts with someone willing to take a chance.

Bucking the Four-Star GeneralsProcter & Gamble limited corporate memos to a single page.

Neil McElroy took a chance in May 1931. At 26, he was managing the ad campaign for P&G’s Camay Soap. He stuck his neck out and wrote his boss a 3-page memo asking for more staff.

In doing that, he laid out new concepts for managing brands. He advocated appointing a “brand man” who would have “full responsibility” for a managing the brand and use rigorous data-driven methods to develop a plan to increase sales.

P&G adopted his approach and became one of the most successful consumer product companies in the world. McElroy’s 800-word memo gave birth to modern brand management.

Not bad for a 26-year-old with a BA in economics. P&G named him president in 1948.

Then, President Dwight Eisenhower, formerly supreme commander of the allied forces in Europe during World War II, wanted someone with superb organizational and communication skills to run the Pentagon.

Skipping over ex-military he picked McElroy for Secretary of Defense in his second term. The former brand man took office on Oct 9, 1957. Five days before, Russia launched the first artificial satellite into orbit.

The term, Sputnik moment, was born.

Just five weeks later, Secretary McElroy went to Capitol Hill to propose the Advanced Research Projects Agency (ARPA), within the Pentagon. He testified that it would have “a function that extends beyond the immediate foreseeable weapons systems of the current or near future.”

McElroy stuck his neck out again. ARPA was an audacious and controversial idea given the way the military was organized.

As it turns out, Congress embraced the idea. However, it still wasn’t smooth sailing.

The Army, Air Force and Navy opposed it. The Joint Chiefs of Staff registered their opposition. So did the Atomic Energy Commission. But the fact that the military hated it, according to one report, made President Eisenhower love it even more.

DARPA (as it is now known) was authorized on Jan. 7, 1958, 96 days after Sputnik. Two days later, in his State of the Union Address, the president introduced the new agency as one of the responses to “harmful service rivalries” from the armed forces.

DARPA evolved into a science-driven entrepreneurial organization that spawned many fundamental technologies that have changed the world. It had some rocky times during the Vietnam War era, and much of its works have focused on top-secret military research. In 1973, with the controversial war behind it, DARPA refocused on “high risk projects of revolutionary impact.” (See “The Pentagon’s Brain” by Annie Jacobsen for more details on the birth of DARPA.)

McElroy didn’t invent the internet, GPS or any other technology. He simply took the risk to push an idea others resisted. That’s what catalysts do. They challenge conventions, bear the weight of failure, and sometimes, when the timing is right, unleash prosperity for everyone else.

Now slow-growing countries say they want ARPAs. What they really need are catalysts.

Making ProsperityEntrepreneurs are the oft-sung heroes behind economic growth. They are the people who take the chance to start a new business. One that may be their financial ruin. Or lead to a good living and possibly even great wealth.

Some build on their own fundamental innovations, like Thomas Edison. Others rely mainly on other’s innovations, like Steve Jobs and Steve Wozniak. Either way, they create new products or cheaper and faster ways to make things. This drives enormously sustained economic growth, and prosperity that lifts most people up.

Many entrepreneurs never become household names. A few months before McElroy’s three-pager, Irma Phillips wrote and starred in the first radio soap opera. She built a business writing many more radio and television daily soap operas, including “Guiding Light” that had a 72-year run. P&G and other brand advertisers funded the soaps. Daily soaps delighted millions of people.

Far more entrepreneurs make small contributions, like the person who starts a small business that fills an unmet need in town, which adds up.

Entrepreneurs and their investors generally get rewards that pale in comparison to the value they generate for everyone else. Others end up mimicking their ideas, like all the copycat Starbucks, or building on them which in turn generates value, like Uber on the iPhone.

Standing on the shoulders of scientists and inventors, entrepreneurs have been behind rapid improvements in prosperity for centuries.

Catalysts Help Poverty Drop Like a StoneOne just has to look at recent times to see evidence of the importance of entrepreneurs, and other catalysts, in driving growth.

Starting in the mid 1980s, country after country embraced markets to drive development and growth. For some countries, such as Vietnam, markets and entrepreneurship were largely new. For others, such as Sweden, governments reduced the role of the state in running industries and curtailed regulations. In many countries, including China, entrepreneurs seized the opportunity.

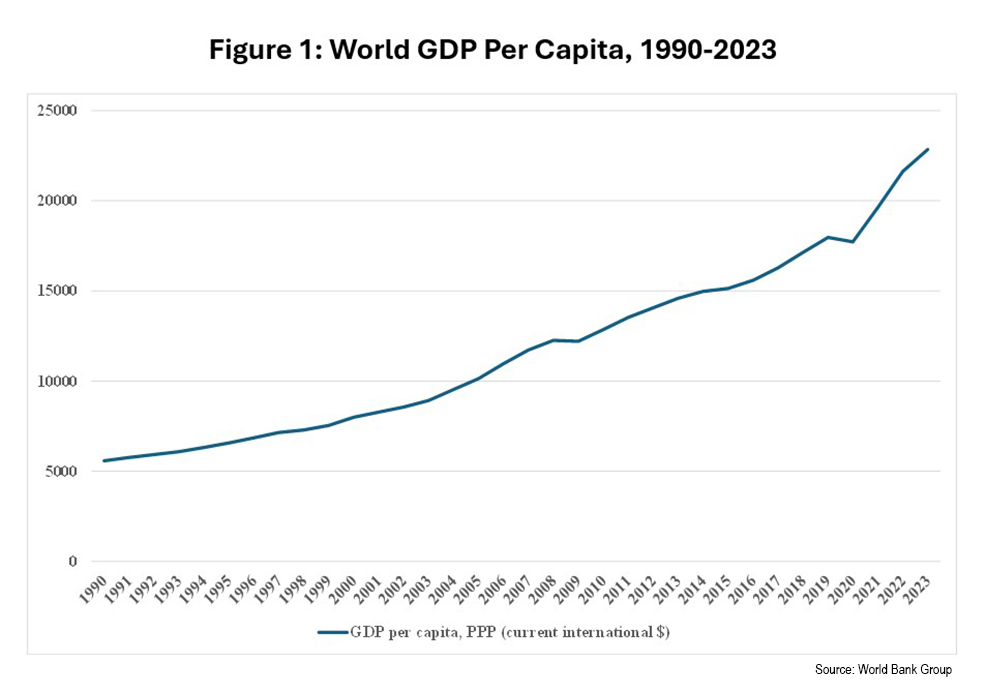

World GDP per capita, adjusting for purchasing power parity, exploded. It increased from $5,578 per person in 1990 to $22,850 per person in 2023 as shown in Figure 1. The percentage of people living in extreme poverty declined from 39.0% in 1989 to 8.1%in 2020. Global trade increased because entrepreneurs help create more things to trade.

Entrepreneurs are important catalysts. They get most of the praise, glory and print.

But many others who take chances, like McElroy, play critical roles. Everywhere, in corporations, government, non-government organizations and elsewhere.

They are critical players in making the world a better place.

Why Stick Your Neck OutIt is nigh impossible to know whether someone who sticks their neck out will come up with a winner unless they give it a try. That goes for the catalyst and everyone they try to persuade to bet on the idea with money or reputation. So why not just play it safe?

Some people are just very confident in themselves. Or optimistic that all the dependencies for success will turn in their favor. Many of them are probably too confident, or too optimistic. For the rest of us, that’s fine. That’s because we will benefit from the things that come about when they take a chance and succeed.

Economists focus on another key reason people take chances. They are risk takers. Risk averse people prefer a certain outcome to a bet that could pay more on average, but could also pay less. They don’t take chances even though they might do very well. Risk takers like the upside. They will take a chance for an upside, rather than a certain payout, so long as the upside is big enough, and even if they might get nothing at all.

Risk taking is central to the economic theory of entrepreneurship and applies to catalysts generally. A number of studies tend to confirm the theory. But it is hard to nail causal relationship between risk taking and entrepreneurship. There are many ways to confuse correlation with causation. A recent empirical study, by Professors Chandal and Ulen, took a clever approach.

The authors looked at whether Americans whose parents were born in a foreign country were more likely to start businesses if risk taking was more prevalent in their parents’ country. The premise is that risk preference is past down culturally in families. They found it did. A higher degree of risk taking in their parent’s country of origin raised the likelihood of starting a business substantially even after controlling for a multitude of other factors.

A significant supply of risk takers is probably a necessary condition for a country to have catalysts who can drive growth.

But risking taking alone isn’t sufficient, because catalysts need to have good ideas that will drive value on average. They are more likely to have better ideas when there is a base of research and innovations they can leverage.

And entrepreneurs are more likely to start businesses if they have greater access to capital, as Boyan Jovanovic and I showed in our 1989 study, which has been widely confirmed.

The Twenty-Year Overnight SuccessIt is easy to conclude that successful catalysts are just smarter than the rest of us. That they really weren’t too confident or overly optimistic. Maybe they like risk, but their idea wasn’t all that risky. They just happened to be right.

At the end of 2012, Nvidia, which was soon to turn 20, had a market cap of $7.7 billion. It had a nice business making high-end chips mainly used in gaming. Stephen Witt’s recent book describes the meeting that changed everything.

One employee, Bryan Catanzaro, saw the future in neural networks. He started building a software library that could accelerate the development of neural networks using Nvidia’s CUDA software platform. He couldn’t get much interest from his colleagues. So he stuck his neck out and made his case directly to the CEO.

It worked. Jensen Huang, the story goes, quickly realized AI would be a once-in-a-lifetime opportunity. He decided to bet the company on AI and asked Catanzaro to accelerate the development effort.

Today, Nvidia’s market cap is $4.3 trillion. He was right.

But that’s only with 20/20 hindsight.

So much could have gone wrong. AI could have sputtered out, yet again, after the initial hype. The deep learning architecture that was critical for GenAI wasn’t revealed until the release of the landmark “Attention Is All You Need” paper by Google researchers in 2017. OpenAI had some ideas, but their LLM could very well have performed poorly. Or someone could have devised innovations that made Nvidia’s technology less important, or the company could have been less successful in improving the hardware and software technologies that the LLMs depended on.

If we roll the clock back, we see how important it is for people to stick their neck out and take chances.

Catanzaro could have been too afraid Huang would bite his head off, and Huang could have decided that the bipolar life of AI, alternating between excitement and despair, still made it too risky to bank on. Sure, their move was genius, but the payoff was hardly guaranteed. Almost all the growth in market cap happened after the launch of ChatGPT in November 2022.

Many catalysts also took chances in 2013, but things just didn’t work out for them. In retrospect they didn’t have such a good idea; the timing wasn’t right; the execution was poor; or the obstacles were just too high. Or they just weren’t lucky in the many things that need to go right.

That leads to a fundamental economic insight into catalysts.

Celebrate the Losers, Honor the MinnowsCatalysts aren’t like runners in a race where the best one wins. The economy needs lots of catalysts to stick their necks out, to take their chances, to uncover the great ideas and launch the businesses that will drive growth and prosperity. That’s because no one really knows they could be a winner unless they try.

As a country, a government or a business we need lots of catalysts. People who have good ideas and will stick their necks out to pursue them.

And that’s why we need to reward people for trying: to get them to stick their necks out in the first place. That can mean outsize rewards like those successful entrepreneurs and their investors get.

But it also means that we need to applaud those who try even when they fail. That’s particularly true in situations, such as in government, where it isn’t possible to give massive rewards for the rare catalyst who makes a massive contribution.

That, of course, begins by encouraging people to try even if they fail, within reason.

Most catalysts won’t be superstars even if they succeed. They will end up running small businesses like someone who starts a boutique that meets a need in a town or a modest factory that makes parts bigger firms need. Individually, they aren’t that important, but collectively they are critical contributors to growth and prosperity. We should applaud them, including those who think big but stayed small, or tried and failed.

Most important, we need catalysts everywhere to grow and prosper.

Driving Long-Term Growth Through CatalystsThe U.S. economy comprises many interlocking parts that work together to create economic growth and prosperity. So do most other countries.

The business sector comprises diverse firms: mature corporations, tech firms (some of which are seeing their age), small businesses, startups, and finance, which ranges from VCs to PE to big banks. Small businesses are collectively big. They account for 43.5% of GDP. The tech sector is important, but even at lofty valuations, it was about a third of the market cap for the S&P500 in September 2025.

No surprise, the government is enormous.

Federal, state, and local spending was 36.5% of U.S. GDP in 2023, including transfer payments, according to the IMF. (GDP includes government spending and investment, excluding transfer payments. It is common to measure the importance of government by comparing government spending, inclusive of transfer payments, to GDP. Exclusive of transfer payments, government spending and investment comprised 17.2% of GDP in 2023.) The government touches the economy in multiple ways, from wasteful regulations to funding scientific breakthroughs. The courts and the legal system are a small part of the cost. Extensive economic research over the last 25 years has found that a robust legal system is a fundamental ingredient for growth.

There’s far more.

Standard setting organizations, for example, solve coordination problems for firms and consumers that create efficiencies and enable new products. They were essential for the widespread adoption of mobile phones, mobile broadband, and the smartphone revolution. Many other nonprofit entities help solve collective action problems and thereby generate growth.

As we saw with McElroy, it is important to have catalysts everywhere.

It is far too simple to say that without McElroy (or Eisenhower) we wouldn’t have an internet, or GPS. We can’t know how technology would have evolved without DARPA and what would have emerged when. He likely made a difference though.

It is also not too rash to conclude that having many people, like McElroy, coming up with ideas and sticking their necks out to push them, generates growth and prosperity.

As with all good things, there are limits. People have bad ideas, sometimes harmful ones, and the pursuit of them may pose risks to all of us. The trick is finding the right balance that encourages enough catalysts who have good ideas to try and succeed.

Slow-growing countries would do well by looking at the supply of catalysts and barriers to having them stick their necks out.

Everywhere. Including in the government.

David S. Evans is an economist who has published more than 10 books and 200 articles, many related to entrepreneurship, platforms, the digital economy, and competition policy. He is the chairman and co-founder of Market Platform Dynamics. He has taught at the University College London and the University of Chicago Law School. For more details, see davidsevans.org. This article is part of Evans’ Catalyst Series and extends insights developed in his book Catalyst Code: The Strategies of the World’s Most Dynamic Companies, co-authored with Richard Schmalensee.

The post Why Economies Need People Willing to Stick Their Necks Out appeared first on PYMNTS.com.