November Issuer Data Extends Trend of Rising Credit Card Delinquencies

Securities and Exchange Commission (SEC) filings from several card issuers offer up a mixed portrait of the U.S. consumer in November.

Delinquency rates were lumpy, though down a bit from October. Charge-off rates were higher, and overall, the data confirm PYMNTS Intelligence’s own findings from this past fall that indicate some struggling with the debt that’s already on the books.

As recently as November, the share of consumers carrying at least some card debt is pervasive, at a cumulative 74.7%. The percentage is fairly static across income levels, but the percentage ratchets up to more than 90% for consumers who live paycheck to paycheck with issues paying bills.

Our surveys show that the average outstanding balance among paycheck-to-paycheck cardholders who have difficulties paying their bills is $7,038, outstripping those who live paycheck to paycheck without such difficulties averaged an outstanding balance of $5,766. Financially stable cardholders averaged $3,202. Roughly 40% of struggling consumers hit their limits with some regularity.

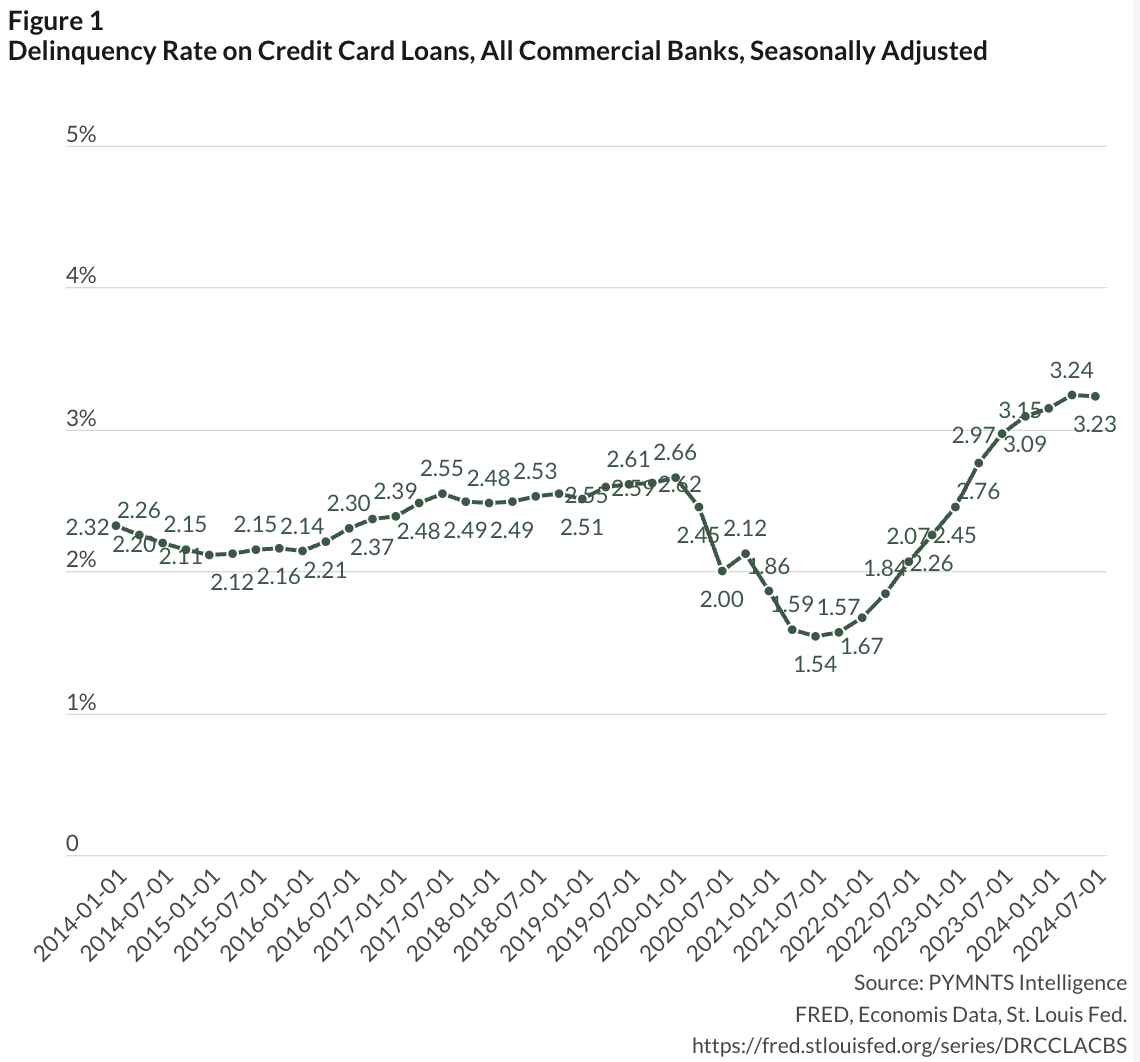

The Bigger PictureWith those stressors in place, and as balances have been rising, the general trend of delinquencies has been captured in the graphic below, where delinquencies are well off their lows of about 1.5% of credit card loans, and as of the end of the third quarter, per the Fed — and across all banks surveyed — the delinquency rate was 3.23% at the end of September.

There’s some evidence of a (small) decline in those rates, as detailed in November’s data, and as measured month over month. The SEC filings for some of the issuers, as referenced above, show some moderation or flattening for some of the marquee names in banking.

For instance, JPMorgan detailed in its filing that 0.87% of its card loans were delinquent in November, which is flat from the previous reading. Bank of America’s data shows a 1.5% delinquency rate, just about from the previous month and up from 1.4% in August. The same percentages are apparent in Citi’s filings.

But the creeping pace of charge-offs may signal a trend that bears greater scrutiny. Charge-offs happen when issuers deem the accounts, with mounting delinquencies, uncollectible and effectively close the account, allowing no future charges to be incurred. These are the accounts that move into collections, and can ultimately prove ruinous to credit scores.

Charge-offs are rising at many of the banks, where BoA’s charge-off ratio was 2.7% in November, up from 2.4% in the previous month. Bread Financial’s charge-off rate was 8%, above the pre-pandemic levels of about 6%. For companies like Capital One, charge-off rates at more than 6% were markedly higher than about 4.4% pre-pandemic.

The Federal Reserve estimated last month that credit card charge-offs at the end of the third quarter were 4.7%. In the third quarter of 2019, that metric stood at 3.7%.

We’re nowhere near the 10% charge off levels that had been a hallmark of the years following the financial crisis of 2008. But with inflation still persistent, credit cards are still being wielded in force to buy everyday essentials. As a result, the pressures of meeting monthly card payments (to say nothing of paying them down significantly) may become even more intense.

The post November Issuer Data Extends Trend of Rising Credit Card Delinquencies appeared first on PYMNTS.com.